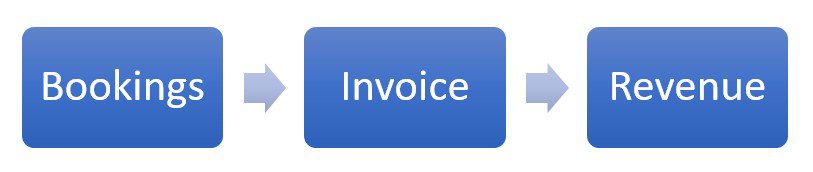

The SaaS revenue cycle all starts with bookings. But what is a booking? And how does a booking differ from invoicing and revenue? SaaS is full of metrics, but in this case, we are mixing SaaS and accounting terminology to make things even more confusing. In this post, I will explain the differences among a booking, an invoice, and revenue.

This SaaS terminology is important for sales, customers success, and the leadership in your organization to understand. I must mention one qualifier, though. If you target mid-market and enterprise deals or sign contracts with your customers, this post is especially relevant for you. If your customers sign up via your website and pay by credit card, the bookings terminology may not be as relevant. But after the bookings process, the revenue cycle follows the same general process.

With that, let’s dive in to see how a booking becomes an invoice and then recognized revenue. I’ll also cover the calculation of contract values.

What is a Booking?

In sales and accounting, you hear a lot of talk about bookings. The SaaS revenue cycle begins with a signed contract between you and your customer. And that’s how I define a booking.

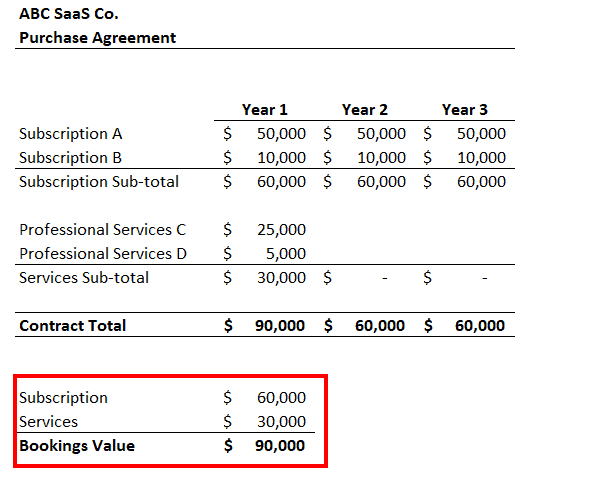

A booking is an executed (signed by both parties) contract between you and your customer for software and/or services.

The contract contains products, pricing, and payment terms among other things. A contract is a customer-facing document, but a it’s a lot like an operating manual for accounting. It tells the accounting team who to invoice, how much, what products, and when.

Once the contract is signed and becomes a booking in your CRM system, the contract is passed on to your accounting team to process. Processes here can vary widely depending on your invoicing and accounting software.

Once the required data is entered in your accounting system, you create the invoice, post it (I’ll explain later), and email it to your customer.

Download my bookings template at the bottom of this post.

How to Measure a Booking

It’s important to note that a booking measures only the first year of the contract. This is where tracking bookings may differ from total contract values. Whether it’s a one-year contract or a multi-year contract, we count only the first year of the software subscription.

Make sure your team is aligned on the calculation of bookings. If your sales team closes a multi-year contract with price increases or additional product in outer years, they may argue that the bookings number should be higher. It’s a valid point but becomes very tricky to track in your CRM by averaging the years of the contract.

We may also have sold more than just software on the contract. If we also offer a professional services component, the entire amount of the services contract value will be counted as a booking.

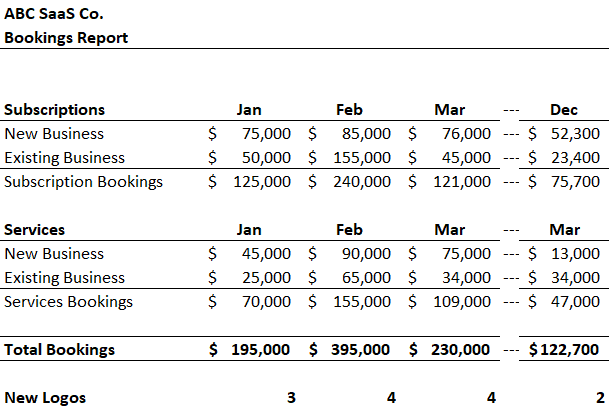

When tracking bookings, I like to separate the first year of a booking into values for subscriptions and professional services. And from there, I further segment bookings into new business versus existing business. I also track logo counts for new business wins.

Bookings to Invoice Process

Your sales team has closed the sale which creates a “closed won” opportunity and a booking (executed contract). Now, your accounting team springs into action.

Accounting receives notice that it’s time to process the new contract.

The customer contract is like an operating manual for accounting. It tells us who we are invoicing, what we are invoicing, and how often we are invoicing.

To invoice the customer properly, accounting will focus on the purchase agreement and the payment terms. It’s important that the pricing and payment terms are clear and concise.

The payment terms dictate a majority of the who, what, and how of invoicing. And just as important, payment terms influence how we recognize subscription and/or professional services revenue.

Contract to Invoice

With information in hand, whether via the contract or contained in your CRM software, accounting will transfer this data to their accounting and invoicing software. If your system allows, I try to automate as much as the invoicing and renewal process as possible. For example, entering the necessary details of a multi-year contract, so that you can “set it and forget it.” Invoices will generate automatically as you run your weekly or monthly invoicing process.

When accounting generates a customer invoice, we “post” it to the general ledger. You could say things become “real” once the invoice is posted to our accounting system. We now have an official financial record and electronic trail of information.

When we post an invoice, we debit accounts receivable (increases receivables) and credit either revenue on the P&L or deferred revenue on the balance sheet. At this point, invoicing is complete, and the revenue recognition process begins.

Revenue

At this point, we have “closed won” the deal, counted it as a booking, and invoiced the customer. Do we have revenue yet? Maybe. I wrote a very detailed post on SaaS revenue recognition, so I’ll summarize the basics below.

Once we have invoiced the customer, the revenue recognition process begins. With the adoption of the new revenue standard, ASC 606 – revenue from contracts with customers in the US, we follow a five-step model for recognizing revenue. There are many technical considerations when recognizing revenue, but for pure play SaaS models, we can boil it down to this.

Generally, if we invoice our customers on monthly terms, our invoicing will equal our revenue. We post the invoice directly to revenue on our SaaS P&L. Revenue recognition is complete.

However, the accounting picture is much different if we invoice in terms longer than one month. Rather than posting the invoice directly to revenue, we must now post the invoice to the liabilities section of the balance sheet. This creates a deferred revenue liability and “parks” the revenue on the balance sheet.

Revenue Recognition Example

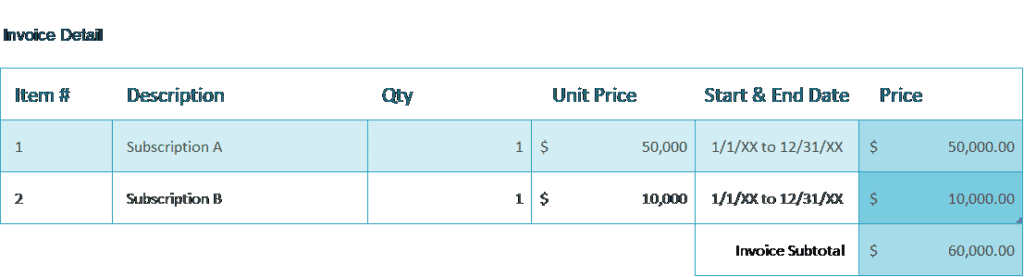

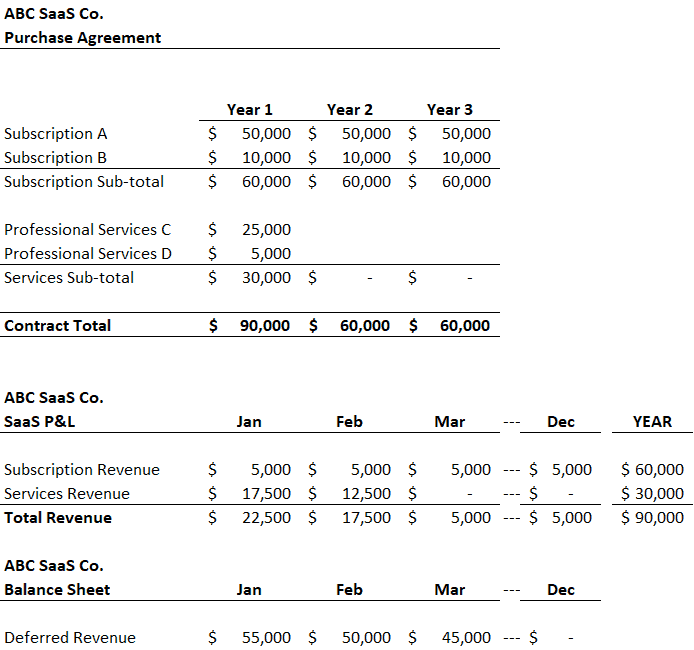

In the example below, we signed a multi-year agreement valued at $210K in total contract value. We invoiced the customer for year one of the subscription (see invoice above). The subscription begins on January 1.

In January, we will recognize $5K of the $60K subscription, or 1/12th. This leaves us with a deferred revenue balance of $55K as of the end of January ($60K year one subscription value less $5K of recognition in January).

The services recognition will depend on how the payment terms were written. Services revenue is often recognized under the percentage-of-completion method or based on recognition milestones.

Revenue as a Liability

Why a liability? Well, with that signed contract or booking, we have created a future obligation to deliver a good or perform a service. Therefore, we create a liability for deferred revenue.

A deferred revenue liability is a a future obligation to deliver a good or perform a service.

As we deliver our software to our customers each month, we are fulfilling our contractual obligation. We can ratably recognize a portion of the revenue each month.

Why is Revenue Recognition Important?

Revenue recognition is critical to SaaS businesses. Maybe, my short introduction to revenue recognition was painful, but proper revenue accounting is critical. You must be able to create an accurate SaaS P&L. And with a proper SaaS P&L, you will better financially manage your SaaS business.

As you scale, your revenue recognition process must be bullet proof.

Without proper revenue recognition, it is very difficult to truly understand the financial performance of your business and produce relevant SaaS metrics. For example, your gross margins will jump up and down each month and revenue-related metrics will be unusable.

SaaS Contract Values

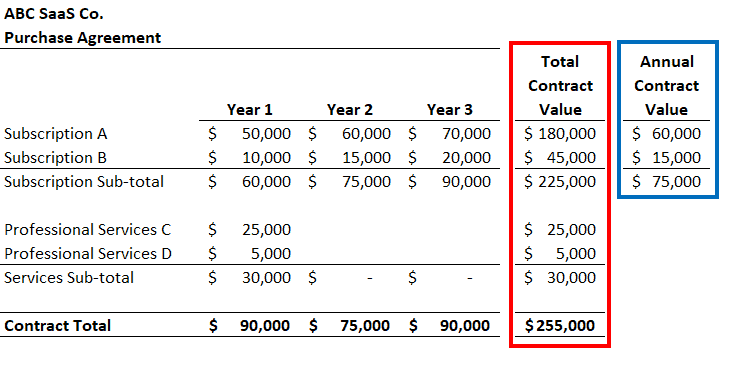

Finally, let’s discuss contract values. Contract values are often quoted in presentations, internal management reports, and are requested in due diligence. It’s important to get this right.

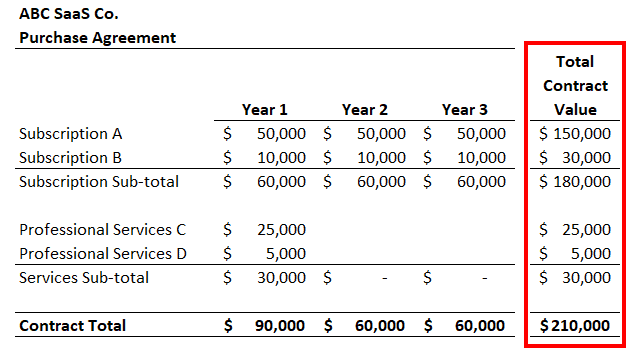

Total Contract Value (TCV)

Total contract value measures the dollar value of all products and services from an executed contract between you and your customer. This includes all years of the contract if it was structured as a multi-year contract.

In pure play SaaS, this is often the value of your subscriptions and professional services, but it should include any sold items from the contract.

The total value of all products and services can be summed as one number, but I always like to differentiate between recurring revenue and one-time items.

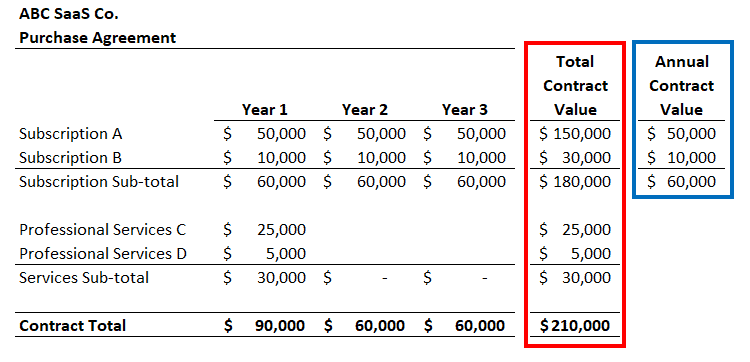

Annual Contract Value (ACV)

Annual contract value measures the first-year value of the contract. It gets a little fuzzy when you think about what products to include in ACV. Do you include subscription revenue and one-time services?

Since we operate a SaaS business, I think in terms of recurring revenue for annual contract value.

The annual contract value below demonstrates the calculation when we have increasing values during the contracted term. In this case, I am averaging the three years of subscriptions and using that as my ACV.

Contract Language Pitfalls

Be careful with contract language that may nullify a multi-year contract. For example, I look for language around optional years, early outs, termination without cause, or contingencies.

This language is often proposed by your customer’s procurement team or legal counsel. If it includes language such as this, make sure you understand what years of the contract are truly contracted and what years may be optional. Only locked in years should be included in total contract value.

Summary

The SaaS revenue cycle begins with bookings, then becomes an invoice, and finally recognized revenue. It’s important to understand the steps in the process, so that you can speak the same language as your accounting and sales teams.

It’s also beneficial when speaking with customers about their contracts and invoicing status. Finally, when you review your P&L, you’ll understand the accounting mechanics behind the revenue section.

Download

I have worked in finance and accounting for 25+ years. I’ve been a SaaS CFO for 9+ years and began my career in the FP&A function. I hold an active Tennessee CPA license and earned my undergraduate degree from the University of Colorado at Boulder and MBA from the University of Iowa. I offer coaching, fractional CFO services, and SaaS finance courses.

Thanks for the walk through Ben especially understanding P&L and Balance Sheet implications.

If for some reason your contract is signed after the start date of the subscription what date do you regard as the booking date – the contract date or the subscription start date?

Hi Harry,

I typically focus just on the bookings month. If the contract signed in December, but the subscription start date was in November, I would still count the booking in December since that will align with the opportunity close date.

Ben

Thank you, Ben.

Dear Ben – thanks for the article. Very helpful as always. I’ve been reading through a lot of your articles and am a fan. I am an investor and have recently gotten more familiar with studying public SaaS companies. The concepts are certainly the same as your written material, but I guess the investing exercise is slightly different than building our own spreadsheet as a start-up. Rather, it is deciphering what the Company disclosed and I’m trying to line it up with your concepts. I would love if you shed some light on a few of these. From a 10Q under a section on “Contract Balances”:

“Contracted but unsatisfied or partially unsatisfied performance obligations were approximately $4.6 billion as of July 31, 2020, which includes $604.6 million in non-cancellable Flexible Spending Account (FSA) commitments from customers where actual product selection and quantities of specific products or services are to be determined by customers at a later date. The Company has elected to exclude future sales-based royalty payments from the remaining performance obligations. The contracted but unsatisfied or partially unsatisfied performance obligations expected to be recognized over the next 12 months are approximately 58%, with the remainder recognized thereafter.”

A couple questions below. It would mean a great deal if you can share your thoughts:

Does this mean $4.6Bn is the RPO (Remaining Performance Obligation), in other words, the Backlog?

Per your article, Total Bookings should only count 1-year obligations, so should that be 58% * $4.6Bn = $2,668mm per your definition?

As an FYI, I was in touch with the Company’s IR team and they noted Deferred Revenue is inclusive in the $4.6Bn (Total Deferred Revenue = $1.5Bn)

Does this mean $4.6Bn – $1.5Bn = $3.1Bn is the portion of RPO that is CURRENTLY unbilled?

To correctly get to the Total Contract Value (TCV), would you add the $4.6Bn with the quarterly sales disclosed or would the right way to think about it be to use LTM sales?

How would one get to New Billings and New Bookings for that quarter? Would New Billings be Deferred Revenue (End of Period) – Deferred Revenue (Beginning of Period)? And New Bookings would be RPO (End of Period) – RPO (Beginning of Period)?

You’re the man. Appreciate your help.

Yes Ben, this work and your other blog content is much appreciated. I am a delivery manager who is often on the edges of these issues, so this is very informative.

Thanks for this wisdom, Ben.

Question: If we book a three year contract, are paid for the three years up-front, and use cash basis accounting, we need to recognize 100% of the revenue when the check is received, correct?

Hi Gary,

Yes, if you are cash basis, you’d post that invoice to revenue. With accrual accounting, you would defer and recognize over time.

~Ben

Ben: This is extremely useful. Have used it internall within the company to get everyone on the same page. really appreciate you putting this together

Hi Ben – if your customer pays you 2 years upfront, would you say your bookings was the full 2 year payment? For example a bootstrapped company doesn’t care as much about MRR as they do cash flow. Hence they would be more focused on the total size of the cheque day 1. And all sales people would have an incentive to ‘book’ as much revenue as possible, irrespective of the number of months/years the deal covers.

Hi Scott,

Regardless of what was paid, I only count first year ARR in my bookings report. Of course, bookings does not always match cash flow and revenue. Yes, if you incent sales to book multi-year deals, they will try to do that.

Ben

Hi Ben. Thanks for a nother great article.

For longer term contracts, eithin Saas model, do we raise Vat and pay over to the Revenue authorities when we raise the invoice, irrespective when the customer pays?

Hi Berend,

If VAT is similar to sales tax in the US, then you will pay VAT based on the taxing authorities timeline. The customer may have NOT paid yet!

Ben